Will the NYSI–NYAD divergence spark a violent positioning unwind in mega-cap tech?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-03-25

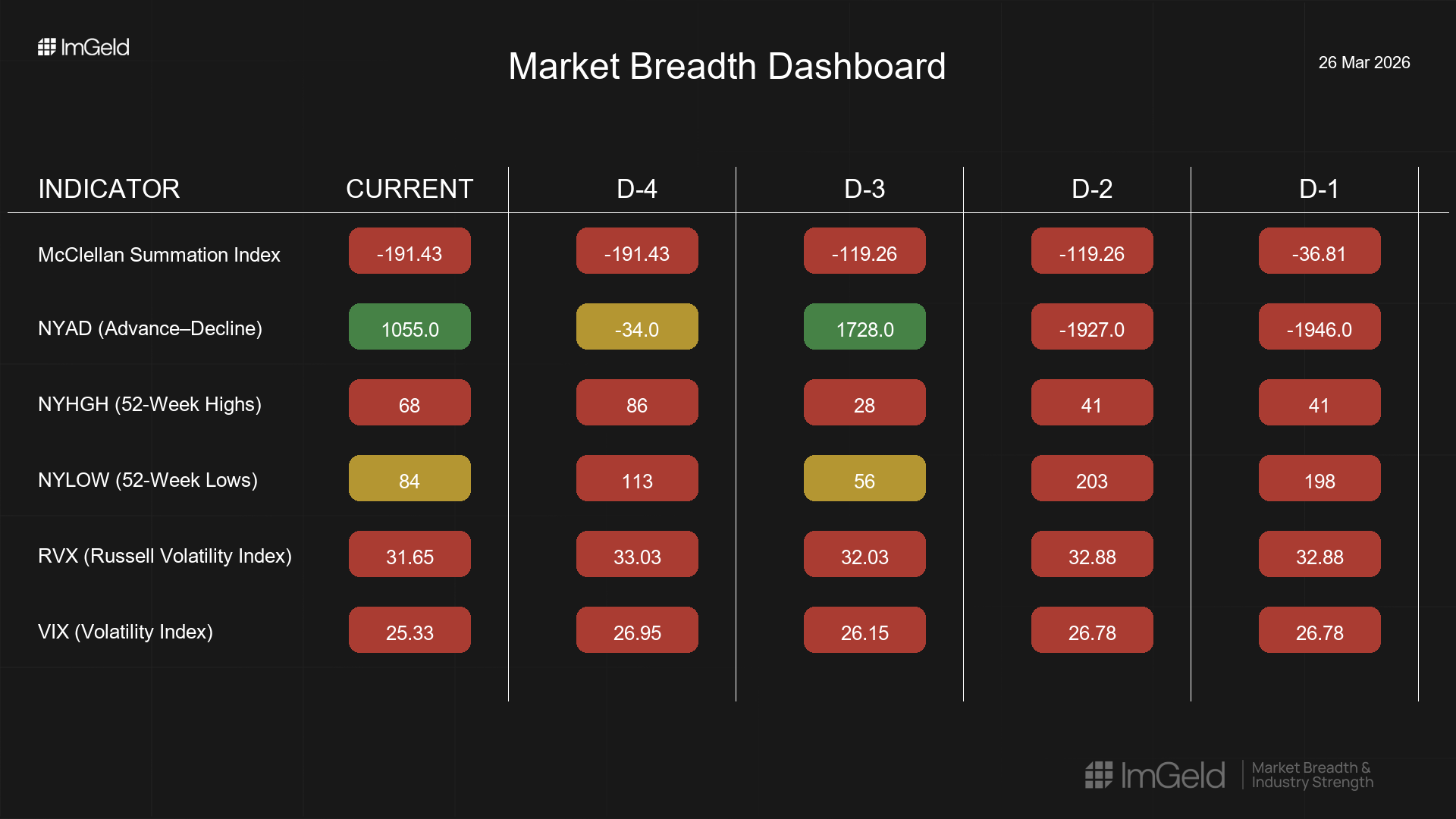

Executive Summary Date: 2026-03-26

Market Bias: Neutral. Allocation: 25% long, 25% short, 50% cash. Breadth over the last five sessions shows a weakening structure with tentative late improvement. NYSI (McClellan Summation Index) fell from -36.8 to -191.4 and then plateaued, signaling a declining trend that has stalled but not reversed. NYAD (Advance–Decline Line) whipsawed from heavy negatives to strong positives, ending mixed but improved late. Volatility remained elevated but eased into the close, with VIX (CBOE Volatility Index) drifting to 25.3 and RVX (Russell Volatility Index) to 31.7. Tactically, selective long opportunities may be emerging in mid-cap industries where new highs are increasing and new lows are receding. Short opportunities remain valid in overowned large-cap industries exhibiting deteriorating breadth and fading momentum. Selectivity remains high.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is attempting to broaden but lacks confirmation, as NYSI is firmly lower while NYAD improved only episodically. Leadership is rotating and remains narrow, with late-week leadership not yet pervasive. Volatility briefly expanded midweek and then compressed into the latest close, still at elevated levels. There is a clear divergence between a declining NYSI and a stabilizing-to-positive NYAD, suggesting short-term accumulation attempts within a weakened intermediate backdrop. By the five-day consistency rule, breadth remains mixed rather than confirmed, pointing to early accumulation attempts that require validation.

Indicator Breakdown

NYSI (McClellan Summation Index) Structure is declining firmly across the period, moving from -36.8 to -191.4 and then stalling. The negative and falling profile argues for caution until a sustained turn higher occurs.

NYAD (Advance–Decline Line) Daily participation was volatile: two heavy down days, a strong rebound, a near-flat negative, then a solid positive. Breadth strengthened late but lacks multi-day consistency.

NYHGH (New 52-Week Highs) Leadership expanded late week, rising from low 30s-40s to 86 then 68. Improvement is constructive but still modest in absolute terms, consistent with selective rather than broad leadership.

NYLOW (New 52-Week Lows) Downside pressure eased from 198-203 early to 84, with a midweek uptick. Risk appetite is improving at the margin but not yet decisive.

Volatility Regime VIX oscillated 26.1-27.0 before easing to 25.3, while RVX ranged 32.0-33.0 before easing to 31.7. Elevated but compressing volatility supports a balanced stance, tight risk controls, and tactical time frames.

Tactical Take

Long: Focus on mid-cap industries showing rising new-high participation and improving breadth, such as select infrastructure software, aerospace suppliers, specialty insurers, and building products.

Short: Large-cap industries with persistent breadth deterioration and crowding remain vulnerable, including mega-cap internet platforms, integrated semiconductors, and broadline retail.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.