Will NYSI/NYAD divergence and RVX premium unwind crowded large-cap leadership next?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-04-07

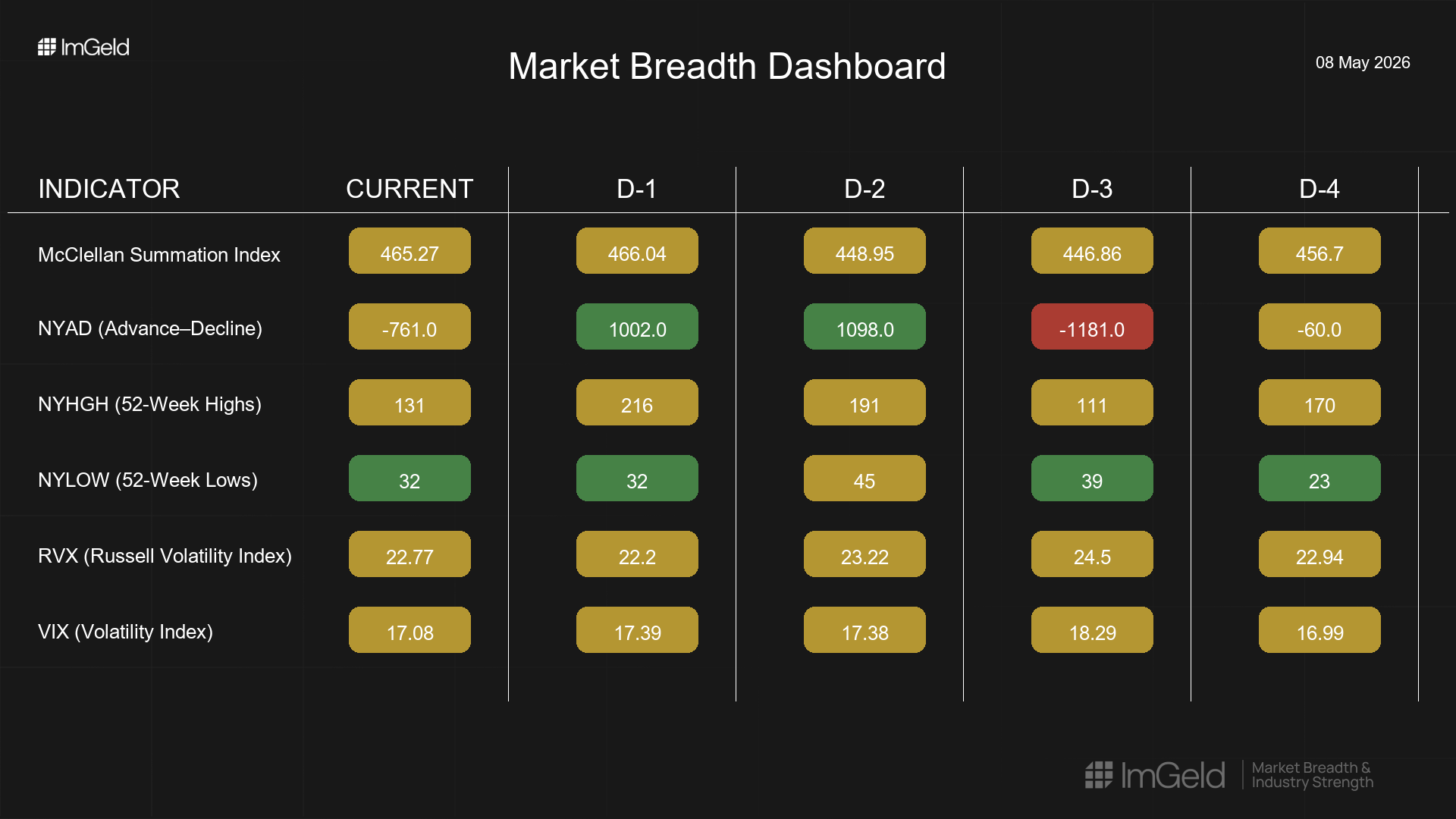

Executive Summary Date: 2026-04-08

Breadth improved modestly over the week with NYSI (McClellan Summation Index) edging higher, but day-to-day participation was choppy and leadership faded into the close of the period. NYAD (Advance–Decline Line) netted slightly positive over five sessions yet alternated between strong accumulation and distribution. Volatility eased from an early-week spike, with VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) both compressing into midweek before a mild uptick in RVX.

Tactically, long opportunities may be emerging in select mid-cap industries where new highs expanded midweek and new lows remained contained, favoring pullbacks rather than breakouts. Short setups remain valid in crowded large-cap industries that stalled as leadership narrowed, particularly where prior momentum softened and breadth rolled over. Selectivity remains high.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation broadened Tuesday to Wednesday, then narrowed Thursday as new highs retreated and NYAD turned negative. Leadership showed rotation rather than sustained concentration, with a brief broadening that did not persist. Volatility compressed from Monday’s spike, supportive of selective risk-taking, but the late-week softening in breadth argues for discipline. A minor divergence persists, with NYSI rising while NYAD was mixed, indicating improving structural tone but uneven daily demand. By the five-day consistency rule, signals remain mixed, pointing to early accumulation that is not yet firmly confirmed.

Indicator Breakdown

NYSI (McClellan Summation Index) Improving. After an early dip, NYSI advanced for two consecutive sessions and finished the week marginally below the high. Structure is constructive, though momentum stalled on the last day.

NYAD (Advance–Decline Line) Mixed. Large positive readings on Tuesday and Wednesday were offset by sizable negatives Monday and Thursday, leaving a small net gain. Participation weakened into the latest session.

NYHGH (NYSE 52-week Highs) Leadership expansion peaked midweek, rising to 216, then pulled back to 131. This indicates tentative, not durable, leadership breadth.

NYLOW (NYSE 52-week Lows) Downside pressure rose early then receded and stabilized around low 30s. Risk appetite is intact, with limited deterioration beneath the surface.

Volatility Regime VIX moved from 18.29 back toward 17.08, while RVX eased from 24.50 to near 22–23 with a slight late uptick. The mild compression supports selective entries, but the RVX premium suggests ongoing sensitivity in smaller capitalizations.

Tactical Positioning

Long: Focus on mid-cap industries with improving leadership and contained lows, such as capital goods, building products, diversified industrial technology, and niche software, using pullbacks and strict risk controls.

Short: Maintain or add in crowded large-cap industries where breadth stalled, including mega-cap application software, semiconductor bellwethers, and defensive consumer staples conglomerates that faded as new highs contracted.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.