Why Disciplined Traders Avoid Holding Positions Through Earnings — And Why Knowing the Date in Advance Changes Everything

Earnings announcements are binary events. Disciplined traders avoid holding through results — structure and process beat conviction every time.

Every quarter, the same dynamic unfolds across equity markets. A stock has been trending, fundamentals look sound, analyst upgrades are accumulating, and then — earnings day arrives. In the hours that follow, price moves 8%, 12%, sometimes 20% in either direction. Traders who held through the report find themselves either celebrating a windfall or managing a position that has just bypassed every stop loss they had in place.

This is not an unusual scenario. It is the structural reality of equity markets during reporting season, and it sits at the heart of why disciplined process-driven traders treat earnings dates as a hard boundary in their exposure management framework.

The question is not whether you have a strong view on a company. The question is whether holding a position through a binary, high-volatility event is consistent with the risk architecture of your portfolio. In most cases — and for most position sizes — it is not.

Earnings Dates as Structural Volatility Events

From a market structure perspective, earnings announcements represent a category of event distinct from ordinary price action. They are scheduled but unpredictable in outcome. The direction and magnitude of the reaction depends not just on reported numbers, but on the delta between actual results and the full distribution of market expectations — a distribution that is never perfectly observable.

What makes this particularly relevant to portfolio management is the concept of gap risk. An earnings announcement typically occurs outside regular trading hours — either before the open or after the close. The stock price does not drift to its new level; it jumps. This means that a stop loss set at a technically meaningful level the night before provides no protection whatsoever. By the time the market opens, the position is already through the stop — often significantly so.

The mechanics are straightforward:

• You hold 400 shares with a stop set 3% below the current price.

• The company reports after hours. Results miss on a key business metric.

• The stock opens 14% lower. Your “stop” triggers at the open price — not your stop price.

• The actual loss is 4.7 times larger than your defined risk.

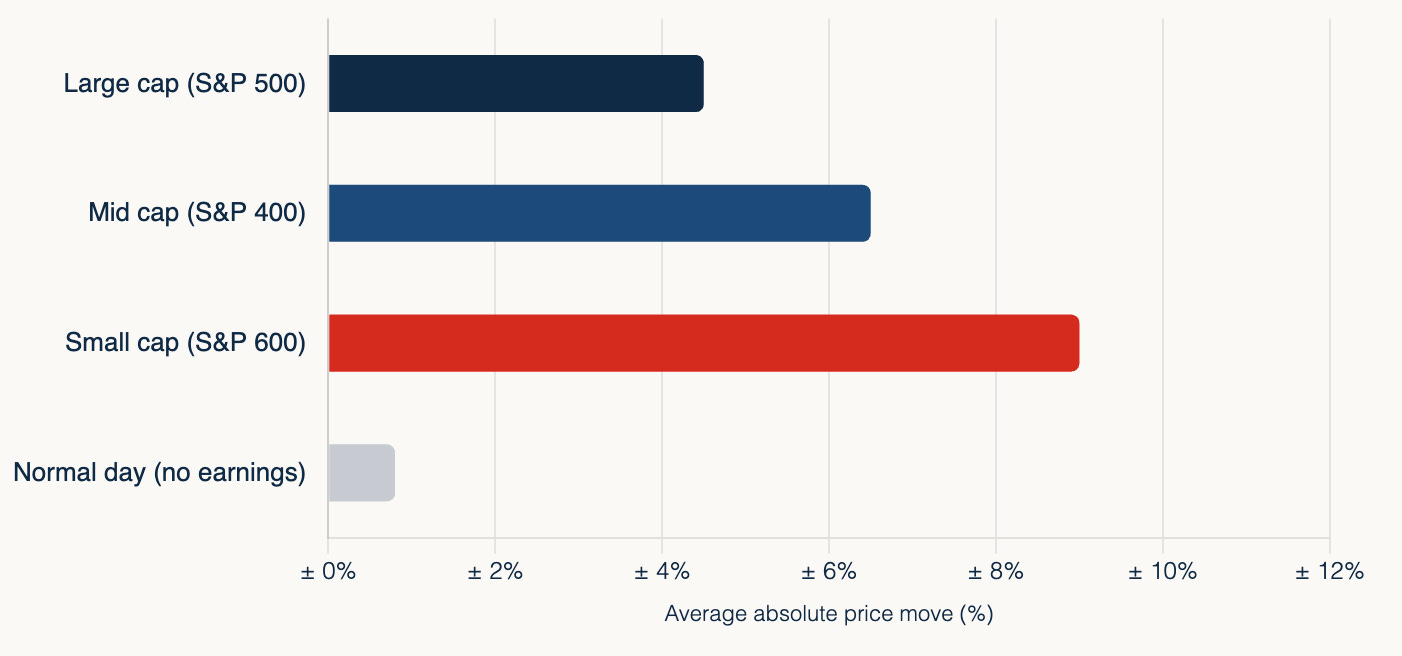

Average absolute price move on earnings day. Source: FactSet Earnings Insight; ATM options straddle implied move.

This is not a failure of execution. It is a structural feature of holding through a binary event. No amount of technical precision in stop placement eliminates gap risk inherent to earnings announcements.

Portfolio Implications: When Risk Cannot Be Bounded

Sound portfolio construction requires that every position carry a defined and bounded risk. This is not a preference — it is the foundational condition that allows a trader to manage multiple positions simultaneously, maintain consistent position sizing, and protect accumulated gains.

An earnings announcement suspends this condition. The moment a position enters the earnings window — typically the final days before the release — the actual risk of the position becomes unquantifiable. Implied volatility in the options market expands sharply, reflecting precisely this uncertainty. The options market is, in effect, pricing the probability distribution of outcomes. Holding equity through that event means accepting the full width of that distribution.

For a portfolio operating with structured risk parameters — maximum loss per trade, maximum portfolio exposure, risk-adjusted position sizing — this creates an immediate problem. A position whose loss cannot be bounded does not fit within a structured risk framework. It is not that the trade idea is wrong. It is that the timing is inconsistent with how risk is supposed to behave in the portfolio.

The appropriate response in most circumstances is clear: reduce or eliminate the position before the earnings window, preserve the gains or cap the loss at a level consistent with your risk parameters, and re-evaluate the position after the announcement when the binary event has resolved and risk is once again quantifiable.

If the thesis is correct — if the fundamentals genuinely support the stock — the opportunity to re-enter will present itself after the announcement. If the thesis was correct and the stock gaps higher, there is still a technically valid entry on the continuation. If the thesis was correct but the stock gaps lower on a short-term miss, the post-earnings environment may offer an even more attractive entry at better valuation. In either case, acting after the event is structurally superior to gambling on the direction of the event itself.

Behavioural Risks: The Conviction Trap

The most common reason traders hold through earnings is not ignorance of the risk — it is conviction. They have done the work. They understand the business. The KPIs are strong. The analyst consensus is positive. The stock is set up technically. Everything aligns. Why exit now?

This is precisely the moment where behavioural discipline becomes the differentiating factor between process-driven traders and those who rely on narrative. The conviction trap works as follows:

• Narrative substitution: A detailed qualitative understanding of the business is mistaken for predictive certainty about the earnings reaction. These are different things. The market reacts to the delta between results and expectations — not to the absolute quality of the business.

• Overconfidence in consensus: Because analyst expectations are publicly visible, traders assume the reaction to a beat or miss is predictable. In practice, a stock can fall on a beat and rally on a miss — the reaction depends on forward guidance, KPI trends, management tone, and the composition of the shareholder base.

• Sunk cost anchoring: Having built the thesis over days or weeks, exiting before the catalyst feels like abandoning work already done. This conflates the intellectual effort of research with the capital risk of the position.

• FOMO on the gap: The possibility of a large positive gap creates a powerful incentive to hold. This asymmetric upside thinking systematically underweights the equally probable downside scenario.

In each case, the underlying error is the same: process has been displaced by narrative. Disciplined risk management does not reward conviction — it rewards structure.

Structural Awareness: Knowing the Date Before It Arrives

One of the most important practical advantages a structured research framework provides is visibility on earnings timing. The risk management logic above is only actionable if a trader knows when the binary event is approaching. Reacting to an earnings announcement after the fact — after the gap has already occurred — is too late.

This is where systematic tracking of earnings dates within a stock research framework becomes operationally critical. At ImGeld, each candidate that passes through the quantitative and qualitative research process is evaluated against a set of structural filters before any position is considered. One of the most operationally useful of those filters is the distance in calendar days to the next earnings release — built directly into the ImGeld Fundamental Report.

The days-to-earnings figure embedded in the Fundamental Report is not a single data point but a set of related inputs that together define the earnings risk window for any candidate under review:

• Days to next earnings (ahead): the raw calendar distance between the current date and the scheduled announcement. A value below roughly 14 days places the stock firmly inside the earnings window — a structural red flag for new position entry.

• Reporting date visibility: whether the date is confirmed or estimated. An estimated date still narrows the window and warrants caution; a confirmed date makes the binary event fully foreseeable and the risk entirely avoidable.

• Fiscal quarter context: knowing which quarter is being reported situates the announcement within the company’s earnings cycle and allows the trader to anticipate whether guidance revision or KPI update is likely — both of which affect the magnitude of the potential reaction.

• Earnings proximity flag at screening level: within the ImGeld process, candidates surfaced through the screener are reviewed against earnings proximity before any trade proposal is constructed. A stock that scores well across valuation, growth, and momentum but is 6 days from reporting does not progress to position sizing — it moves to the radar, pending the resolution of the binary event.

The practical consequence is a clean separation between active candidates — stocks where the full risk management framework can be applied — and watch list positions, where the research work is done but capital is held back deliberately until the earnings window closes. This distinction is not a limitation of the process. It is the process working exactly as intended.

Maintaining this separation also generates a practical edge. Traders who track earnings dates systematically arrive at the post-announcement environment already prepared. They know the thesis, they understand the KPIs, they have price targets defined. When the report resolves and the structural condition is restored — risk quantifiable, gap eliminated, new price level established — they can act with precision rather than scrambling to understand a company they have never researched.

The ImGeld Fundamental Report is updated on a regular cycle, ensuring that the earnings proximity data remains current as reporting windows shift across the calendar. This is particularly relevant during peak earnings seasons — typically the four to six weeks following quarter-end — when a large proportion of the opportunity set enters the binary event window simultaneously, compressing the universe of actionable ideas and raising the importance of selectivity.

This focus on structural layers — earnings timing, sector leadership, participation quality, valuation relative to peers — is consistent with the broader analytical approach described in the ImGeld Industry Rating framework, which contextualises individual stock selection within the underlying strength or weakness of the industries in which those stocks operate.

Process Over Conviction — Every Time

The case for avoiding positions through earnings is not a case against doing fundamental research. Quite the opposite. The research is what allows you to identify the right idea, understand the right valuation, and time the right entry — before or after the binary event, in conditions where risk can actually be managed.

What the research does not do is eliminate the structural asymmetry of an overnight gap. No amount of qualitative depth, no earnings call transcript analysis, no KPI dashboard reduces the gap risk inherent in holding equity through a scheduled binary event outside market hours.

The trader who exits before earnings and re-enters on strength after a confirmed beat is not being timid. They are being structurally intelligent. They have preserved their capital for a moment when the risk is defined, the direction has been confirmed, and the position can be sized with precision.

That is what process-driven trading actually looks like in practice. Not the absence of conviction — but the disciplined subordination of conviction to structure. Because in markets, structure survives. Narratives do not.

References

1. CME Group — Understanding Implied Volatility and Event Risk in Equity Markets

2. NYSE Research — Earnings Season Volatility Patterns and Market Participation

3. CBOE — VIX Methodology and Single-Stock Implied Volatility Around Earnings

4. BIS — Market Microstructure and Price Discovery Around Scheduled Announcements

5. NBER — Earnings Announcements and the Components of the Bid-Ask Spread (Working Paper)