VIX/RVX compress, NYSI sub-zero; are mid-cap breakouts real or a head fake?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-04-13

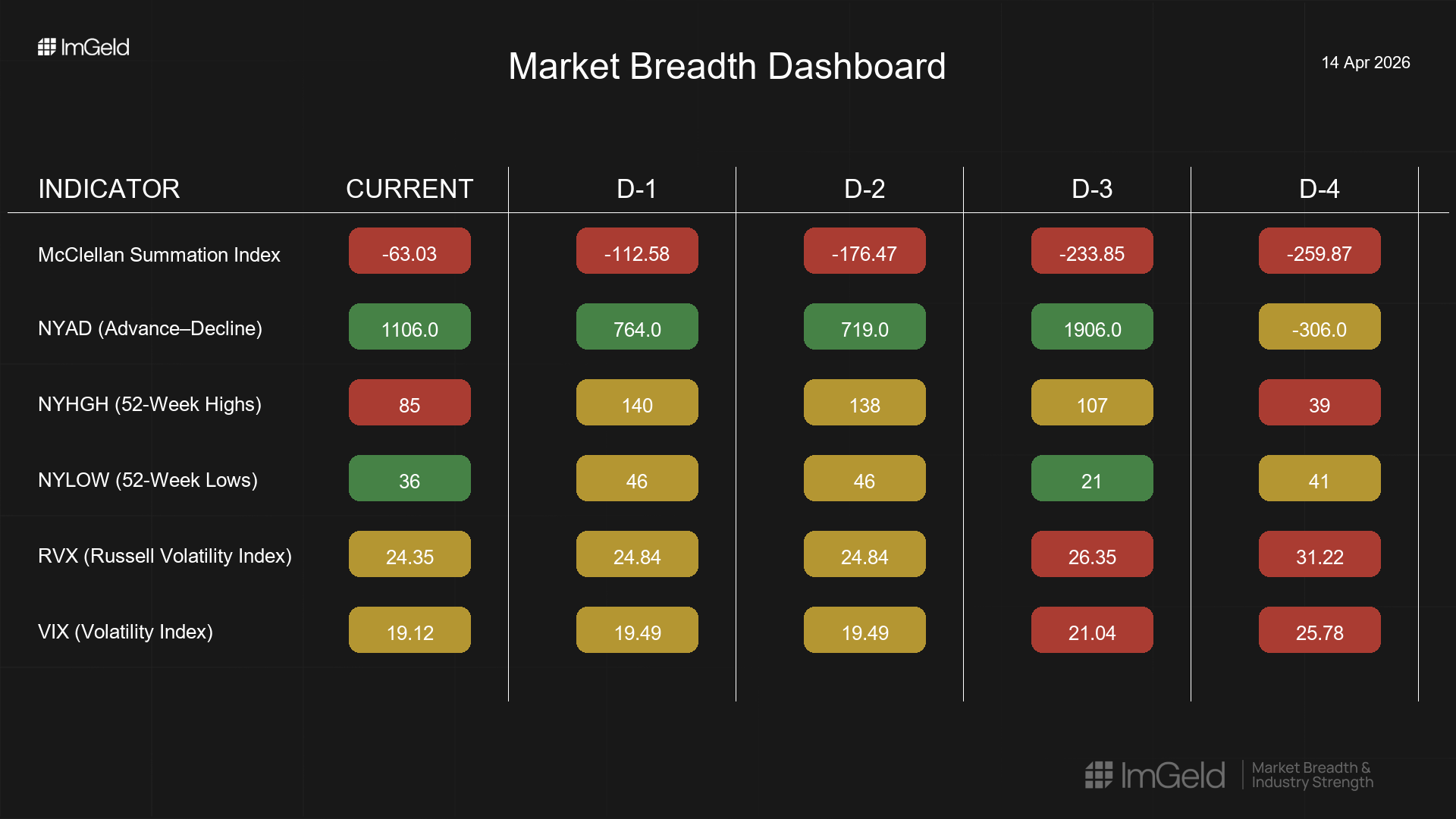

Executive Summary Date: 2026-04-14

Breadth has improved steadily over the last five sessions. NYSI (McClellan Summation Index) advanced from deeply negative to less negative, signalling an early inflexion, though still below zero. NYAD (Advance–Decline Line) posted four consecutive positive days, confirming accumulation. Volatility compressed, with VIX (CBOE Volatility Index) near 19 and RVX (Russell Volatility Index) near 24, supportive of risk-taking with strict selectivity.

Tactically: prioritise high-quality mid-cap (3–10B) industries where new highs persist, and daily advances outpace declines. Short setups remain valid in crowded large-cap leadership and lagging large-cap defensive industries. Maintain discipline, given NYSI remains sub-zero.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is broadening: four straight positive NYAD prints and a clear improvement in NYSI trajectory indicate accumulation. Leadership is tentatively rotating, with an uptick in new highs suggesting expanding winners, though the pullback in new highs on the final day points to still-fragile leadership. Volatility is compressing across both VIX and RVX, reducing downside tail pricing and favouring controlled risk deployment. A constructive divergence is present: NYAD strength contrasts with an NYSI that, while improving, remains negative. By the five-day consistency rule, breadth is firmly improving, but the pattern characterises early accumulation rather than a confirmed uptrend.

Indicator Breakdown

NYSI (McClellan Summation Index) Five-session climb from -259.87 to -63.03. Structure is improving decisively but remains below zero, consistent with an early-phase recovery. A sustained move through zero would confirm the trend.

NYAD (Advance–Decline Line) Progressed from -306 to four consecutive positives (1906, 719, 764, 1106). Daily participation is strengthening, with consistent net advancing breadth indicating buyers are returning beyond a narrow cohort.

NYHGH (New 52-Week Highs) expanded from 39 to 140 before easing to 85. Leadership is broadening, though the late-session fade implies the advance is not yet dominant across industries.

NYLOW (New 52-Week Lows) Contained between 21 and 46, finishing at 36. Downside pressure remains moderate and is receding, consistent with improving risk appetite.

Volatility Regime VIX fell from 25.78 to 19.12; RVX declined from 31.22 to 24.35. This compression supports selective deployment on the long side and improves carry for hedges; however, low-vol regimes are vulnerable to abrupt reversals, warranting ongoing protection.

Tactical Focus

Long: Select mid-cap industries showing persistent breadth thrust and improving new-highs participation, such as industrial machinery, building products, and software infrastructure.

Short: Overextended large-cap leadership and lagging large-cap defensive industries where momentum is deteriorating, and breadth remains narrow.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.