VIX sub-20, breadth mixed—accumulate mid-cap pullbacks; fade overextended large-cap leaders now

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-02-23

Executive Summary Date: 2026-02-24

Breadth improved over the last five sessions with NYSI (McClellan Summation Index) advancing for four days before flattening, while NYAD (Advance–Decline Line) remained net positive despite midweek noise. Volatility compressed as VIX (CBOE Volatility Index) fell below 20 and RVX (Russell Volatility Index) eased after a brief uptick. The backdrop supports a tentative long bias with selective risk-taking. Tactically, emerging long opportunities favor mid-cap industries showing improving participation and earnings resilience, with an emphasis on pullback entries rather than breakouts given modest new-high expansion. Short setups remain valid in overextended large cap index leaders where breadth confirmation is lacking and momentum is stalling.

Get the Industry He3at Map — delivered by email only.

Global Read

Participation is modestly broadening late in the period, but leadership remains concentrated as new highs failed to exceed early-week levels. Rotation appears tentative rather than decisive, with quality and cyclicality gaining incrementally. Volatility is compressing, which typically allows incremental accumulation but also raises the risk of sharp mean reversion on negative catalysts. A mild divergence existed early as NYSI trended higher while NYAD chopped, but this narrowed into week’s end. By the five-day consistency rule: volatility compression is firmly in place; breadth expansion remains mixed; accumulation is tentative.

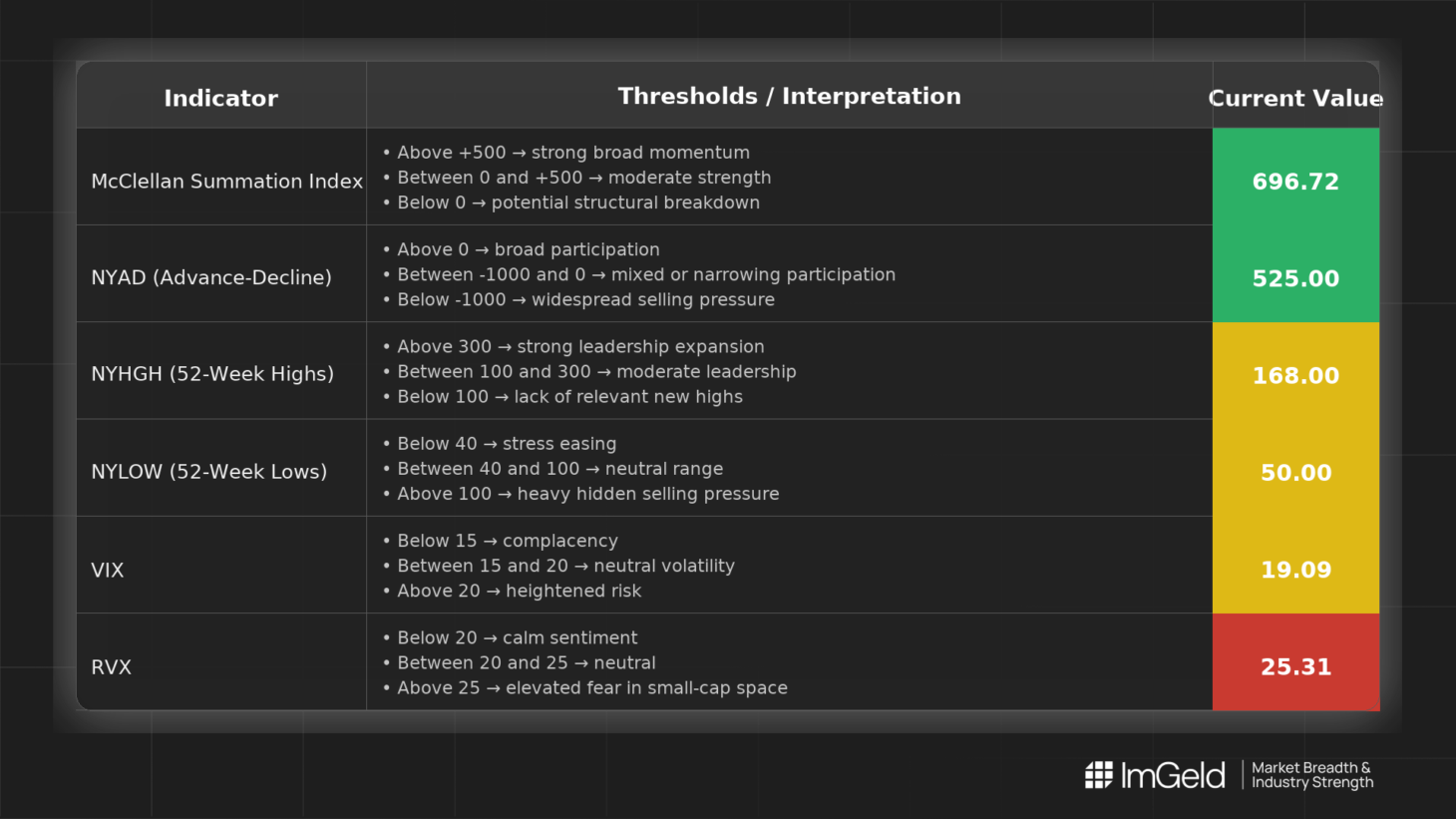

Indicator Breakdown

NYSI (McClellan Summation Index) Structure improved steadily from 649.9 to 696.7 over four sessions, then plateaued. The uptrend remains intact, but momentum is decelerating, arguing for selective adds rather than aggressive chasing.

NYAD (Advance–Decline Line) Daily participation was volatile: strong positive, then soft, a brief negative, followed by a strong rebound. Net breadth is constructive, but the pattern is not yet a firm, multi-day advance.

NYHGH (New 52-Week Highs) New highs contracted midweek (192 to 136) and only partially recovered (168). Leadership expansion is muted, indicating gains are concentrated and breakouts require confirmation.

NYLOW (New 52-Week Lows) Lows remained contained (33 to 64 range, ending at 50). Downside pressure is limited, consistent with stabilizing risk appetite, though not indicative of a decisive risk-on surge.

Volatility Regime VIX declined from 20.6 to 19.1, signaling compression and improved tactical conditions for adding risk on weakness. RVX rose midweek to 26.4 before easing to 25.3. The RVX-VIX gap remains elevated, implying smaller capitalization risk premia persist; positioning should remain measured and event-aware.

Tactical Takeaway

Longs: Prioritize mid-cap industries where participation is improving and fundamentals support durability, such as industrial technology, specialty materials tied to project backlogs, and select application software and healthcare services. Favor pullback entries and breadth-confirmed breakouts.

Shorts: Large cap leaders that are extended with weakening momentum and lack of new-high confirmation remain candidates for tactical fades, particularly in crowded growth franchises.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.