RVX premium persists—does compressing VIX mask imminent risk in large-cap leaders?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-03-011

Executive Summary Date: 2026-03-12

Breadth weakened across the last five sessions. NYSI (McClellan Summation Index) declined persistently, while NYAD (Advance–Decline Line) stayed negative with only a brief mid-period stabilization. Volatility tone eased, with VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) compressing but remaining elevated versus recent months. Selectivity is paramount. Long opportunities, if any, are highly selective within mid-cap industries showing relative strength and improving lows-to-highs profiles. Short setups remain valid in large-cap leadership industries displaying distribution and contracting new highs.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is firmly narrowing: new highs contracted and daily advance–decline remained net negative. Leadership is thinning rather than rotating, with fewer industries producing breakouts. Volatility is compressing in a downtick, which can be deceptive given deteriorating breadth. A minor divergence appeared midweek as NYAD became less negative while NYSI continued to erode, underscoring weakening internal momentum. The five-day pattern points to continuation of distribution, not early accumulation, with the consistency rule favoring a firmly cautious interpretation.

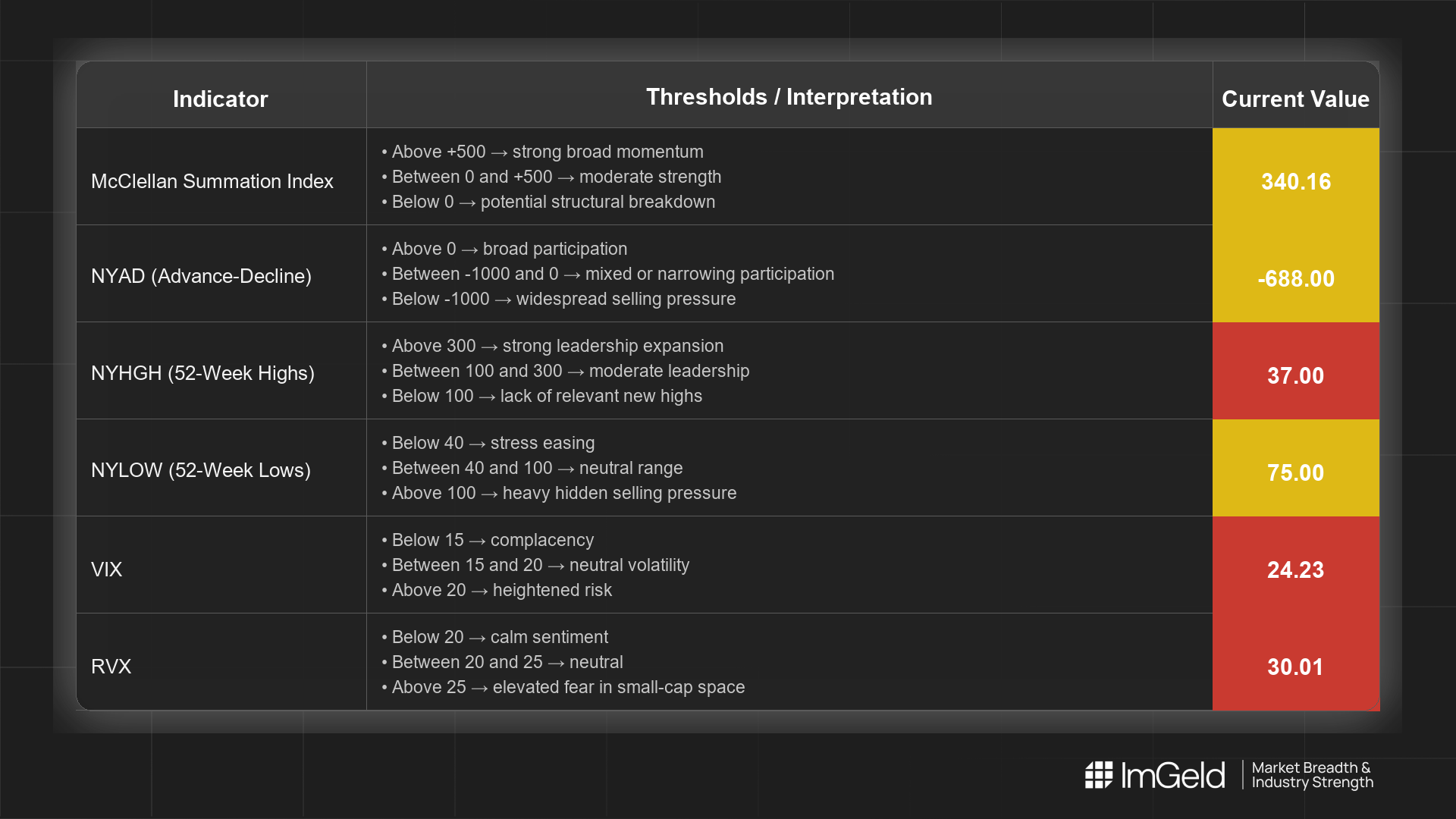

Indicator Breakdown

NYSI (McClellan Summation Index) Structure is declining: 598.43 to 340.16 over the period, with only one flat session. The downtrend signals sustained loss of internal momentum and absence of a base.

NYAD (Advance–Decline Line) Daily participation remained negative each day: heavy negatives early, a tentative improvement mid-period, and renewed deterioration into the last print. Overall breadth is weakening, not broadening.

NYHGH (New 52-Week Highs) Leadership expansion contracted from 58 to the high 30s. Fewer industries are generating fresh breakouts, indicating concentration risk and waning upside sponsorship.

NYLOW (New 52-Week Lows) Lows spiked (124) before easing and then re-accelerating to 75, reflecting persistent downside pressure and fragile risk appetite. Elevated lows argue against aggressive risk-on.

Volatility Regime VIX fell from 29.49 to 24.23 and RVX from 32.63 to 30.01, signaling short-term compression. The RVX premium to VIX persists, implying higher perceived risk in smaller capitalizations. Tactically, compressed volatility alongside weakening breadth favors maintaining hedges and fading overstretched bounces rather than chasing strength.

Tactical Take

Long side: Focus only on mid-cap industries with improving relative breadth (rising highs, contained lows) and defensible cash flows; patience and strict risk controls are essential.

Short side: Large-cap momentum industries showing distribution and shrinking highs (e.g., consumer internet, semiconductors) remain suitable for opportunistic shorts on rallies.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.