NYSI sliding, NYAD mixed—are crowded large-cap growth rallies distribution into strength?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-04-18

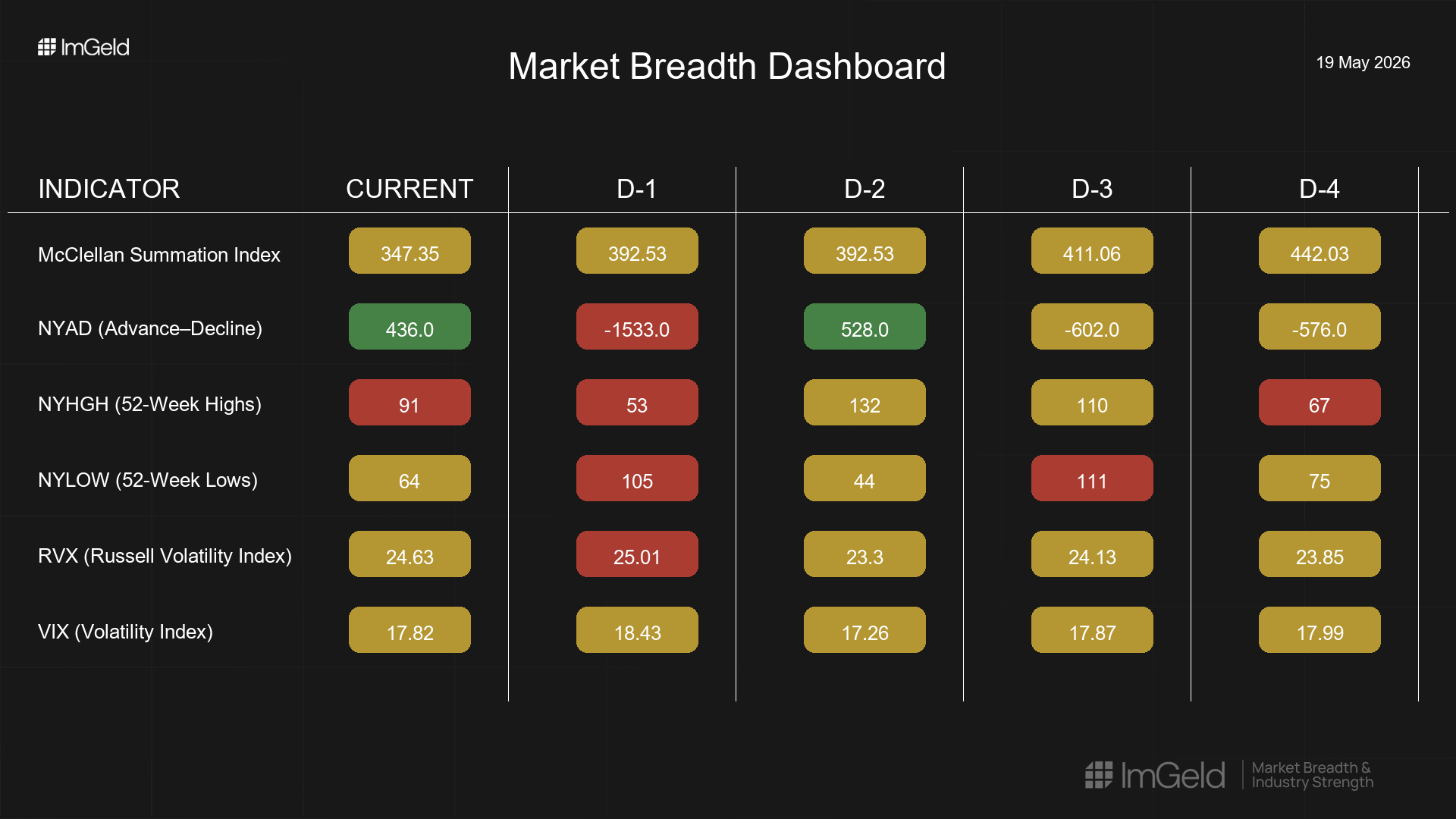

Executive Summary Date: 2026-04-19Summary Breadth softened over the last five sessions. NYSI (McClellan Summation Index) declined from 442 to 347, signaling intermediate deterioration. NYAD (Advance–Decline Line) was volatile and net negative, with a sharp down day on 2026-05-15 offsetting intermittent positives. VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) remained contained in the high-teens to mid-20s, with brief expansion that faded by the latest session. Long opportunities may be emerging only in selective mid-cap industries where new highs are holding and lows remain subdued. Large-cap short setups remain valid in crowded growth industries showing waning leadership and negative breadth. Selectivity is high.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is narrowing as NYSI declined on four of five sessions and NYLOW spiked twice, while leadership is becoming more concentrated: NYHGH peaked midweek and faded before a tentative rebound. Volatility remains contained with episodic expansion; there is no regime shift, but the tape is two-way. A mild divergence is present: NYAD produced two up days, yet NYSI kept rolling over, suggesting rallies are being sold. Five-day pattern: NYSI is firmly weakening (2–5 day consistency), NYAD remains mixed, and volatility remains contained. Overall read points to continuation risk rather than early accumulation; attempts at breadth repair are tentative.

Indicator Breakdown

NYSI (McClellan Summation Index) Firmly declining: 442.03 → 411.06 → 392.53 → 392.53 → 347.35. Intermediate momentum is eroding; a reversal would require multiple strong breadth days.

NYAD (Advance–Decline Line) Mixed and volatile: -576, -602, +528, -1,533, +436. Participation is fragile with downside shocks dominating the five-day net.

NYHGH (New 52-Week Highs) Leadership expansion faltered: 67 → 110 → 132, then down to 53, modest rebound to 91. Improvement is tentative, concentrated in select pockets.

NYLOW (New 52-Week Lows) Downside pressure remains episodic: 75 → 111 → 44 → 105 → 64. Spikes indicate risk appetite is inconsistent; not a capitulation profile.

Volatility Regime VIX: 17.99, 17.87, 17.26, 18.43, 17.82. RVX: 23.85, 24.13, 23.30, 25.01, 24.63. Both indices show contained volatility with brief expansion. Tactically, this supports selective risk-taking in stronger mid-cap industries while keeping dry powder for dislocations.

Tactical Implications

Longs: Focus on mid-cap industries demonstrating relative strength and stable highs-to-lows profiles, such as industrial automation and components, building products, specialty materials, life science tools, and infrastructure software. Selectivity and staggered entry remain key.

Shorts: Remain tactical and selective in large caps within over-owned growth industries where breadth has deteriorated, such as semiconductor design and internet media, particularly into strength.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.