Is VIX compression masking fragility as NYSI climbs but NYAD stalls?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-04-27

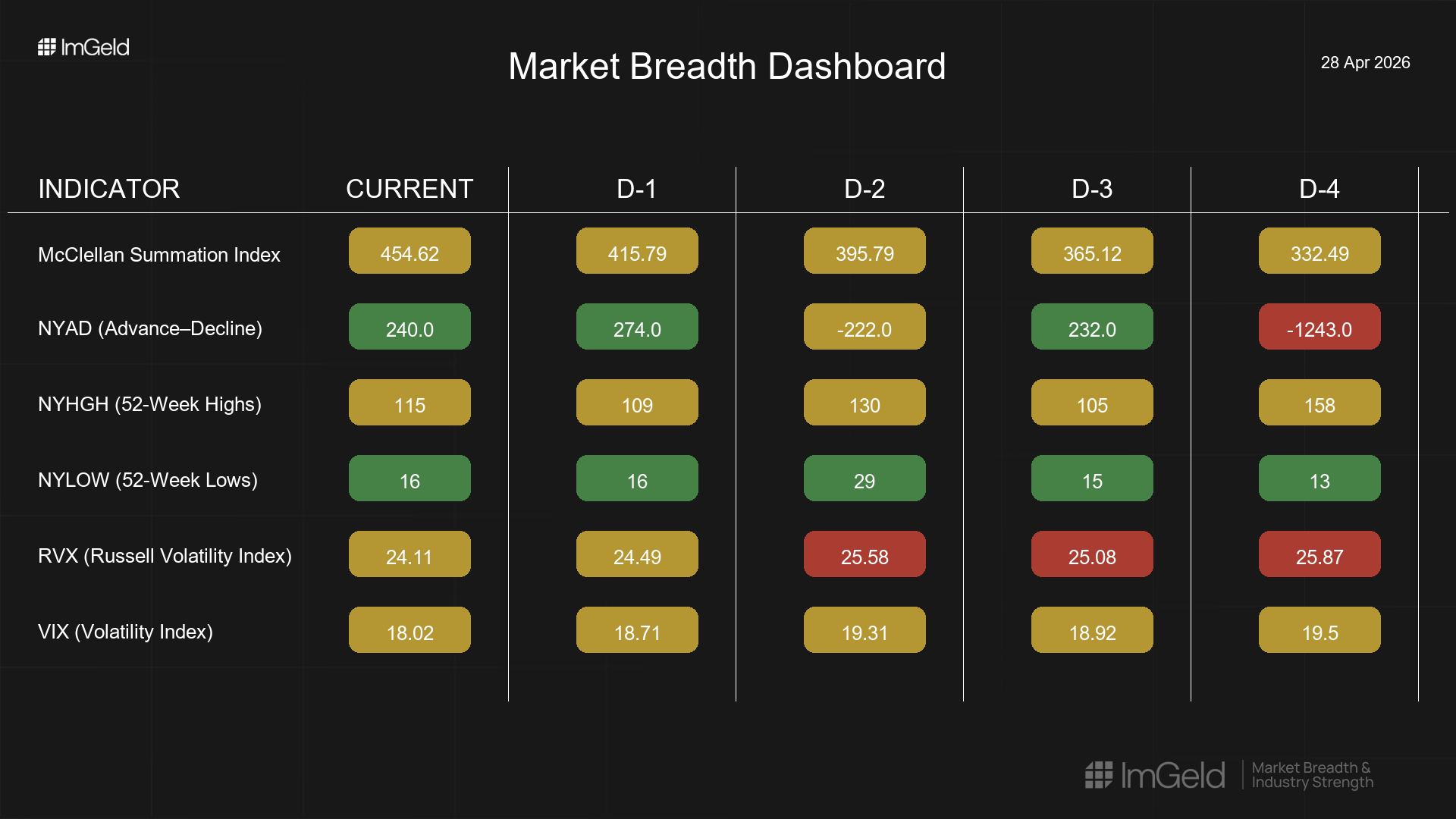

Executive Summary Date: 2026-04-28

Breadth improved over the last five sessions, led by a steady rise in NYSI (McClellan Summation Index) while NYAD (Advance–Decline Line) delivered mixed but net negative prints, turning positive in the final two sessions. Volatility eased, with VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) both compressing. New highs were steady but not expanding, and new lows remained contained. The tape supports a tentative long bias with high selectivity: emerging opportunities in quality mid-cap industries; short setups remain valid in stretched large-cap leadership where breadth is narrowing.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is broadening modestly: NYSI is firmly higher for five consecutive sessions, but NYAD remains mixed, indicating uneven day-to-day participation beneath a strengthening intermediate structure. Leadership remains concentrated; NYHGH is not breaking out, signaling limited leadership expansion, while NYLOW stays contained, consistent with risk appetite stabilizing. Volatility is firmly compressing, reducing downside tail intensity but raising the risk of abrupt reversion if breadth fails to confirm. Divergence: NYSI’s persistent advance versus a choppy NYAD suggests early accumulation under the surface rather than full-throttle momentum. Five-day pattern: NYSI firmly improving; NYAD remains mixed; volatility firmly compressing. Net read: early accumulation, constructive but selective.

Indicator Breakdown

NYSI (McClellan Summation Index) Rising each day (332.5 to 454.6), signaling a firmly improving intermediate breadth backdrop and increasing odds that dips get bought.

NYAD (Advance–Decline Line) Daily prints were mixed: -1243, +232, -222, +274, +240. While net negative over the five-day window, the last two positive sessions suggest improving participation at the margin. Overall, breadth remains uneven.

NYHGH (New 52-Week Highs) 158, 105, 130, 109, 115. Leadership expansion is modest and inconsistent. The absence of a clear uptrend in highs argues for selectivity rather than broad beta.

NYLOW (New 52-Week Lows) 13, 15, 29, 16, 16. Lows remain contained despite a midweek uptick, indicating limited downside pressure and supportive risk appetite.

Volatility Regime VIX eased from 19.5 to 18.0; RVX from 25.9 to 24.1, a firm compression. This supports carry and breakout attempts, but with NYAD still mixed, position sizing and stop discipline remain critical.

Tactical Take

Longs: Focus on mid-cap industries where participation is stabilizing and relative strength is improving, including aerospace and defense suppliers, building products, specialty chemicals, and software infrastructure. Favor pullbacks into rising support over breakouts in thin tape.

Shorts: Select large caps within crowded leadership in the internet, semiconductor, and integrated energy industries remain vulnerable to mean reversion given narrow leadership and compressing volatility. Fade strength into prior resistance.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.