Is the NYSI/NYAD divergence a buy signal for mid-caps or a trap?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-04-06

Executive Summary Date: 2026-04-07

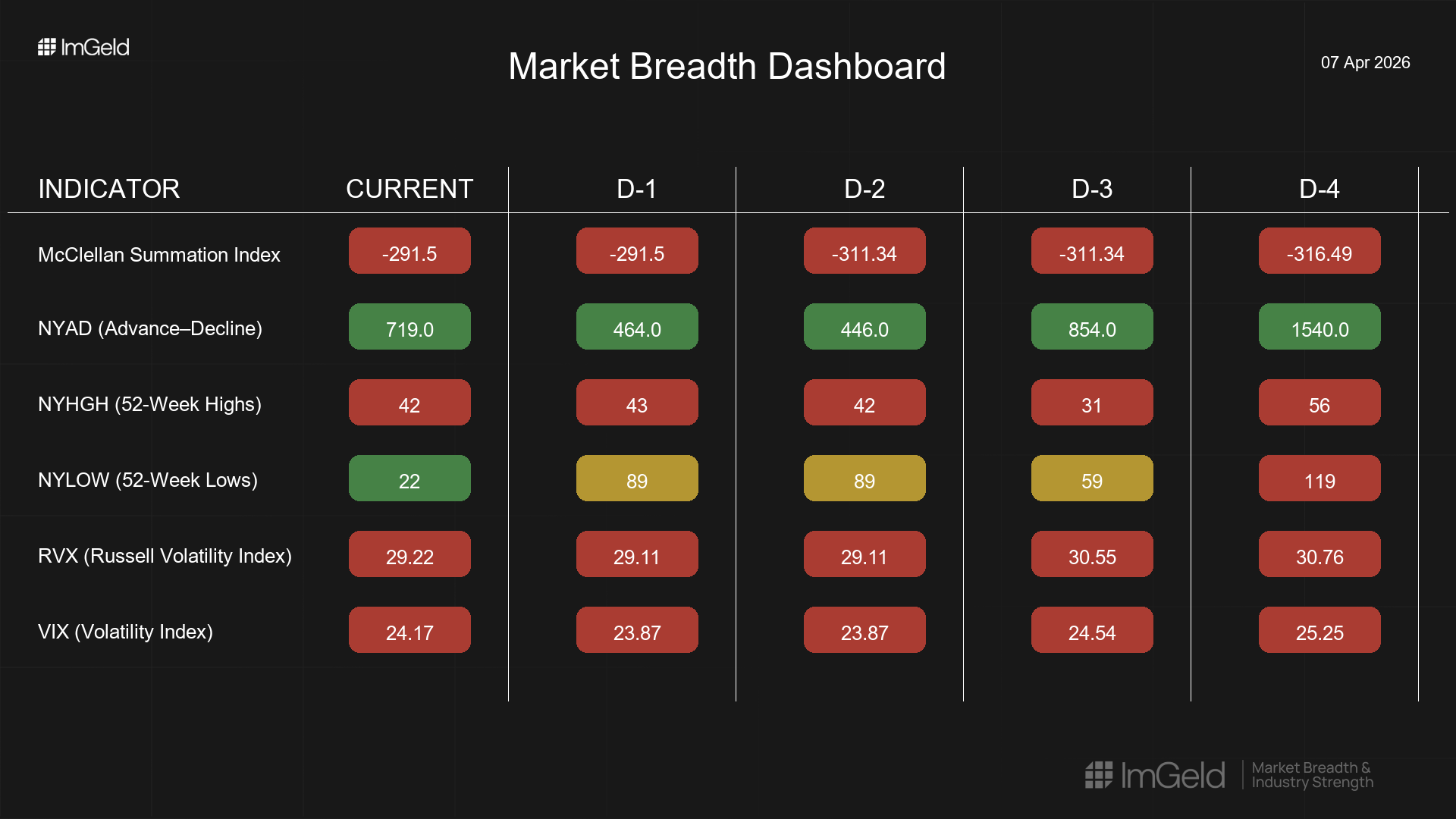

Breadth improved off late-March weakness and then stalled. NYSI (McClellan Summation Index) rose from -316 to -291 across the window and flattened, while NYAD (Advance–Decline Line) stayed positive but decelerated through mid-period before a modest rebound. Volatility compressed into the weekend with VIX (CBOE Volatility Index) hovering in the mid-20s and RVX (Russell Volatility Index) near 29, signalling risk premium remains, but tail risk is not escalating.

Tactically, selective mid-cap long opportunities are beginning to emerge in industries showing persistent net advances and declining new lows. Short opportunities remain valid in overextended large-cap leadership where breadth is narrow and momentum is tiring. Selectivity remains high.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation firmed from the March trough but narrowed mid-week before stabilizing, indicating a tentative broadening rather than a wholesale turn. Leadership is not convincingly expanding, with new highs steady in the low 40s and concentrated rather than diffuse. Volatility has compressed modestly yet remains elevated, keeping risk control relevant. A mild divergence exists as NYSI trends higher while NYAD’s pace cooled, reflecting improving structure but slower day-to-day follow-through. The five-day pattern signals early accumulation, tentatively, not a confirmed continuation.

Indicator Breakdown

NYSI (McClellan Summation Index) Improving then plateauing. The move from -316 to -291 suggests internal repair, but two flat sessions indicate the advance is losing momentum and needs confirmation.

NYAD (Advance–Decline Line) Consistently positive (1540, 854, 446, 464, 719) with a mid-period fade and late-session stabilization. Breadth is constructive but not forceful; participation is improving at a slower rate.

NYHGH (New 52-Week Highs) Muted leadership expansion (56, 31, 42, 43, 42). The rebound from the mid-week dip is modest, implying leadership remains concentrated and has not broadened across multiple industries.

NYLOW (New 52-Week Lows) Downside pressure eased materially, falling to 22 by the last session after oscillating earlier. This supports improving risk appetite and underpins a selective long bias in sturdier mid-cap groups.

Volatility Regime VIX drifted from 25.25 toward 23.87 before a slight uptick to 24.17; RVX followed a similar path to 29.22. Compression without capitulation favors incremental risk deployment, but elevated absolute levels argue for maintaining hedges and disciplined entry points.

Tactical View

Long: Focus on mid-cap industries exhibiting stable advances and falling new lows, where pullbacks are being bought and volatility is diminishing relative to peers.

Short: Maintain selective shorts in overowned large-cap leadership and in industries with persistently weak breadth and elevated new lows on rallies.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.