Is NYAD’s rebound bait while NYSI bleeds and VIX compression lures late longs?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-03-016

Executive Summary Date: 2026-03-17

Breadth weakened across most of the five-session window with a late-day improvement. NYSI (McClellan Summation Index) fell steadily, while NYAD (Advance–Decline Line) printed four consecutive negatives before a strong positive close today. Volatility spiked midweek and eased into the close, keeping risk conditions elevated but improving.

VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) peaked midweek and compressed into today, indicating a tentative reduction in risk premia.

Tactically, selective long opportunities may be emerging in resilient mid-cap industries showing rising new highs and limited new-low participation. Large-cap short setups remain valid in crowded, momentum-heavy industries on failed bounces while volatility stays above long-term medians. Selectivity is high.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation has firmly narrowed over the period, with leadership becoming more concentrated in a smaller cohort, printing new highs despite broad negative advances–declines midweek. Volatility expanded early and then tentatively compressed. A divergence is present: NYSI continued to decline while NYAD turned positive today, hinting at early accumulation but not yet a regime change. By the five-day consistency rule: deterioration in NYSI is firmly in place; NYAD weakness was firm until today’s rebound; volatility compression is tentative; leadership concentration remains. The five-day pattern signals tentative early accumulation within an ongoing corrective phase, not a confirmed turn.

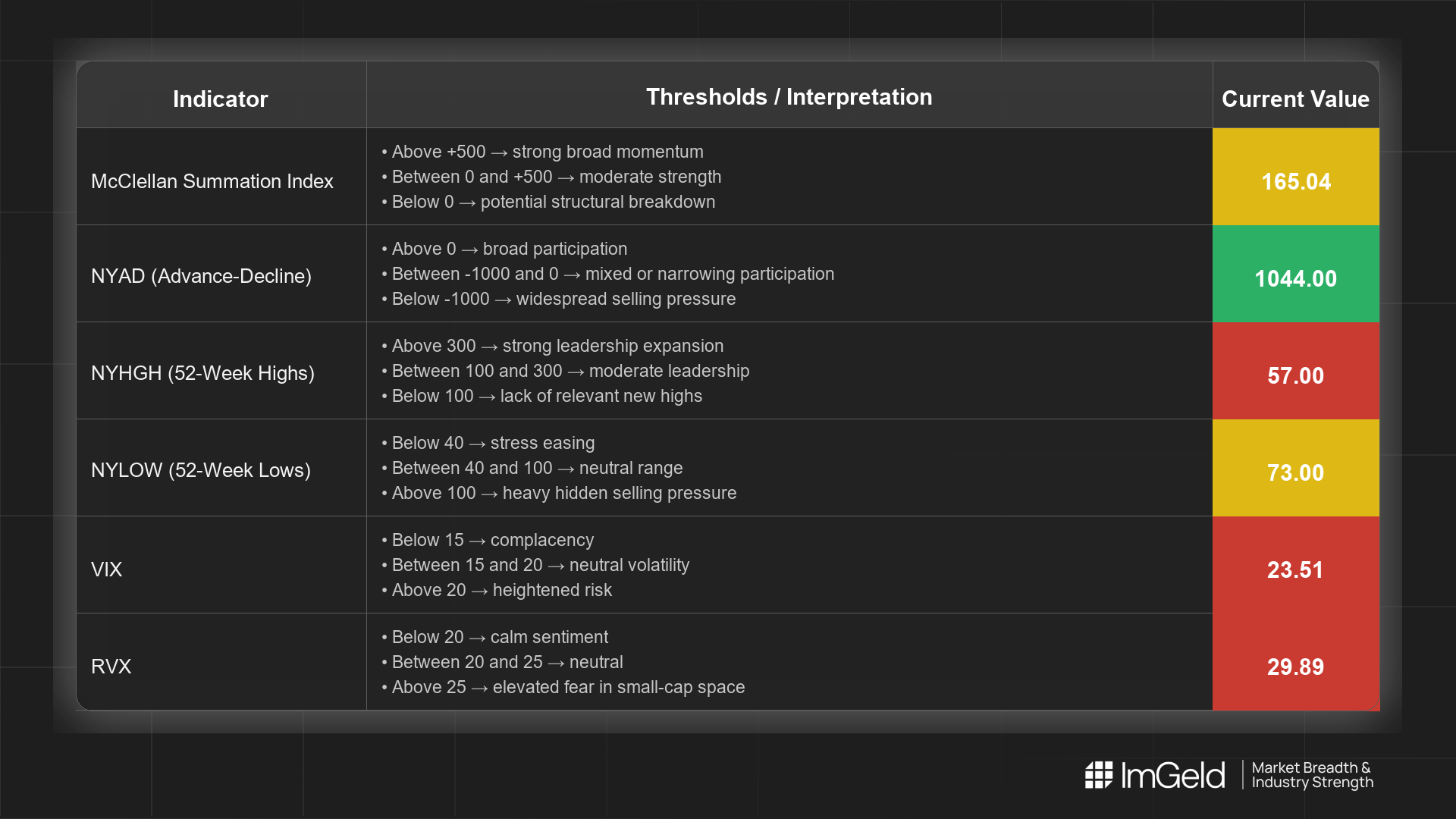

Indicator Breakdown

NYSI (McClellan Summation Index)

Down from 467.56 to 165.04 over five sessions, with only a brief pause. Structure is firmly declining, indicating negative intermediate breadth momentum and a fragile foundation for rallies.

NYAD (Advance–Decline Line)

Prints: -127, -688, -1574, -663, +1044. Participation weakened decisively through 3/13 and improved meaningfully today. On a five-day basis, breadth remains net negative but stabilising.

NYHGH (New 52-Week Highs)

36, 37, 62, 42, 57. Leadership expansion is uneven but improving versus the start of the period, suggesting a narrow leadership cohort is asserting relative strength.

NYLOW (New 52-Week Lows)

38, 75, 121, 104, 73. Downside pressure rose midweek and eased into today, but lows remain elevated versus highs, keeping risk appetite constrained.

Volatility Regime

VIX moved 24.93, 24.23, 27.29, 27.19, 23.51; RVX 30.40, 30.01, 32.84, 33.02, 29.89. The midweek spike followed by a pullback signals tentative compression from elevated levels. This favours staggered entries and tight risk controls over aggressive exposure.

Tactical Takeaway

Longs: Focus only on selective mid-cap industries with improving relative strength and participation, such as Speciality Chemicals, Life Sciences Tools, Application Software, and Waste & Environmental Services.

Shorts: Large-cap opportunities remain in overcrowded, momentum-driven industries (for example, Semiconductors and Interactive Media) on failed rallies if volatility re-expands.

cess the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.