Does the RVX premium confirm distribution while selective mid-cap highs bait late buyers?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-03-30

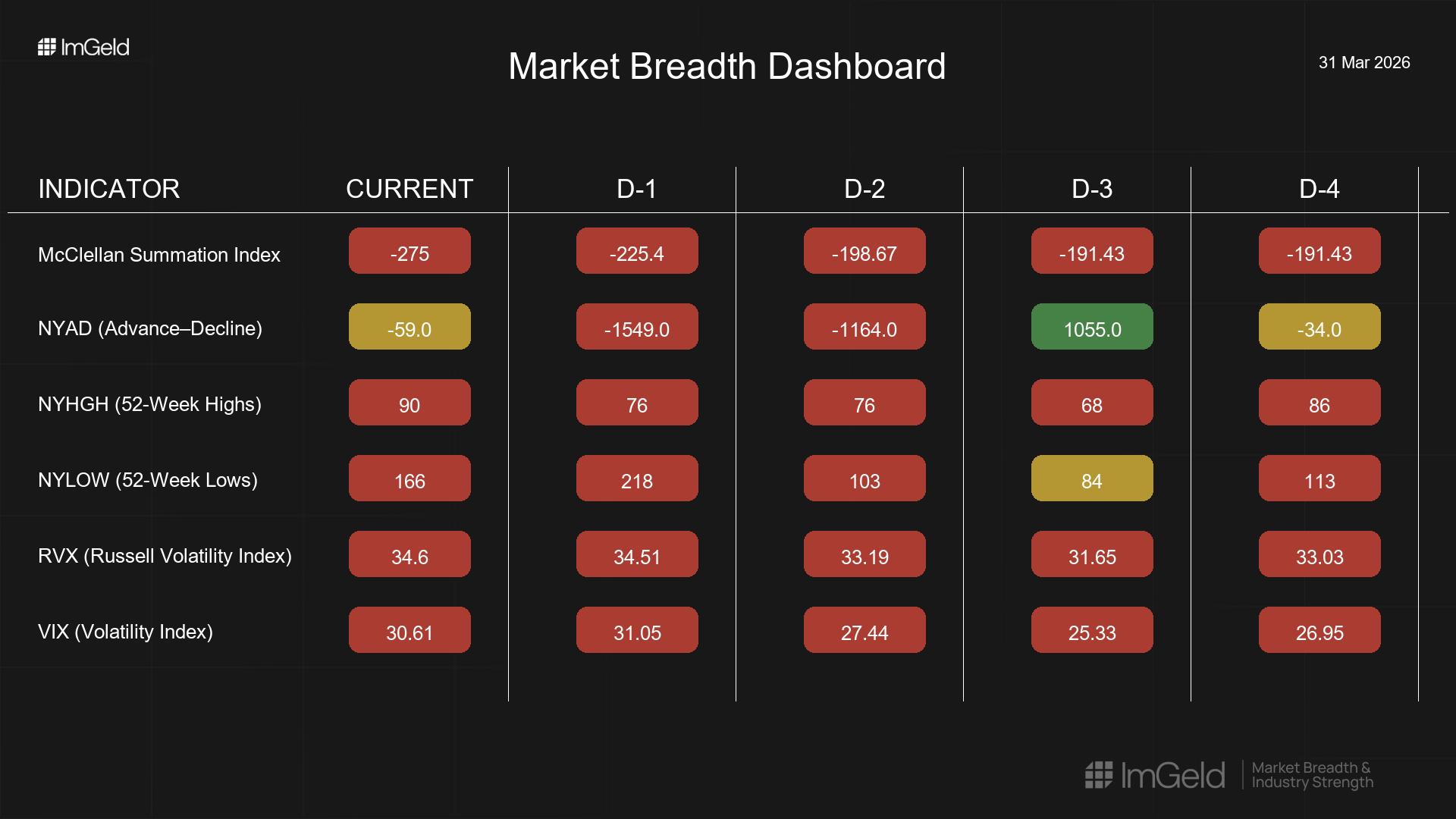

Executive Summary Date: 2026-03-31

Breadth weakened over the last five sessions. NYSI (McClellan Summation Index) slid deeper negative, while NYAD (Advance–Decline Line) posted four down days out of five. Volatility expanded, with VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) holding in the low-to-mid 30s. NYHGH (New 52-Week Highs) stayed modest and stable; NYLOW (New 52-Week Lows) rose and remain elevated.

Tactically, any long opportunity is highly selective and confined to mid-cap industries showing persistent relative strength and steady new highs. Short setups remain valid in large-cap leadership where participation is deteriorating and volatility is amplifying trend risk.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is narrowing: lows rose sharply mid-period and remain elevated, while highs are only inching higher. Leadership is becoming more concentrated, with resilient pockets mostly defensive and quality-focused; there is no evidence of broad leadership expansion. Volatility is firmly expanding, with both VIX and RVX lifting, and the Russell volatility premium signaling disproportionate pressure on smaller capitalizations. NYSI’s persistent deterioration contrasts with a marginal uptick in NYHGH, a narrow divergence that suggests rotation rather than a broad turn. By the five-day consistency rule, breadth weakness is firmly in place (four of five days negative on NYAD; NYSI down), while the single strong NYAD day is an isolated, tentative improvement. The pattern signals continuation of distribution, not exhaustion; any accumulation is early and localized.

Indicator Breakdown

NYSI (McClellan Summation Index)

Declining. From -191.43 on 3/24–3/25, it fell to -198.67 (3/26), -225.40 (3/27), and -275.00 (3/30), confirming worsening intermediate breadth and rising downside momentum.

NYAD (Advance–Decline Line)

Weakening participation. Daily readings: -34 (3/24), +1,055 (3/25), -1,164 (3/26), -1,549 (3/27), -59 (3/30). Four negative sessions, with the largest downtick on 3/27, indicate sellers remain in control despite one strong up day.

NYHGH (New 52-Week Highs)

Modest and narrow leadership. Prints of 86, 68, 76, 76, 90 show stability with a small uptick into 3/30, consistent with selective strength rather than broad expansion.

NYLOW (New 52-Week Lows)

Elevated downside pressure. Lows moved 113, 84, 103, 218, 166, signaling persistent risk aversion even after the mid-period spike.

Volatility Regime

VIX rose from 26.95 to 31.05 before easing to 30.61; RVX advanced from 33.03 to 34.60. This is an expanding and elevated regime. The persistent RVX premium implies continued stress for smaller and mid-cap universes, demanding tight risk controls and staged entries.

Tactical Takeaway

Longs: Only consider highly selective mid-cap opportunities in resilient industries such as defense electronics suppliers, waste services, and specialty chemicals with demonstrated pricing power and rising highs.

Shorts: Large-cap exposures remain attractive where leadership is faltering, notably in internet platforms, megacap semiconductor manufacturers, and consumer discretionary leaders showing weakening breadth and rising volatility.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.