Breadth Broadens, Volatility Compresses: Prioritize Mid-Cap Accumulation Before Confirmation Arrives

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-02-25

Executive Summary Date: 2026-02-26

Breadth is cautiously constructive but not confirmed. NYSI (McClellan Summation Index) stalled early, then slipped into the close of the period, while NYAD (Advance–Decline Line) printed four straight positive sessions, indicating short-term accumulation despite a softer intermediate curve. Volatility eased as VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) compressed, improving the risk backdrop.

Tactical stance: maintain a selective, Tentative Long bias, prioritizing mid-cap industries showing expanding new highs and persistent net advances. Short opportunities remain valid in overextended large-cap, index-heavy franchises and defensives where breadth is narrowing. Selectivity is high; emphasize pullbacks in mid-cap leaders over broad beta.

Get the Industry He3at Map — delivered by email only.

Global Read

Participation is broadening at the margin: NYAD strength and rising NYHGH point to improving inclusion beyond the prior leaders. Leadership is rotating toward a wider cohort, with signals consistent with mid-cap cyclicals and quality growth within technology-linked and industrial industries. Volatility is compressing across both large- and mid-cap proxies, supportive of accumulation windows. There is a clear divergence as NYSI edged lower while NYAD improved, typical of early accumulation phases that require confirmation. Applying the five-day consistency rule, mixed signals within the window mean the bias remains Tentative, with improving odds if NYSI stabilizes.

Indicator Breakdown

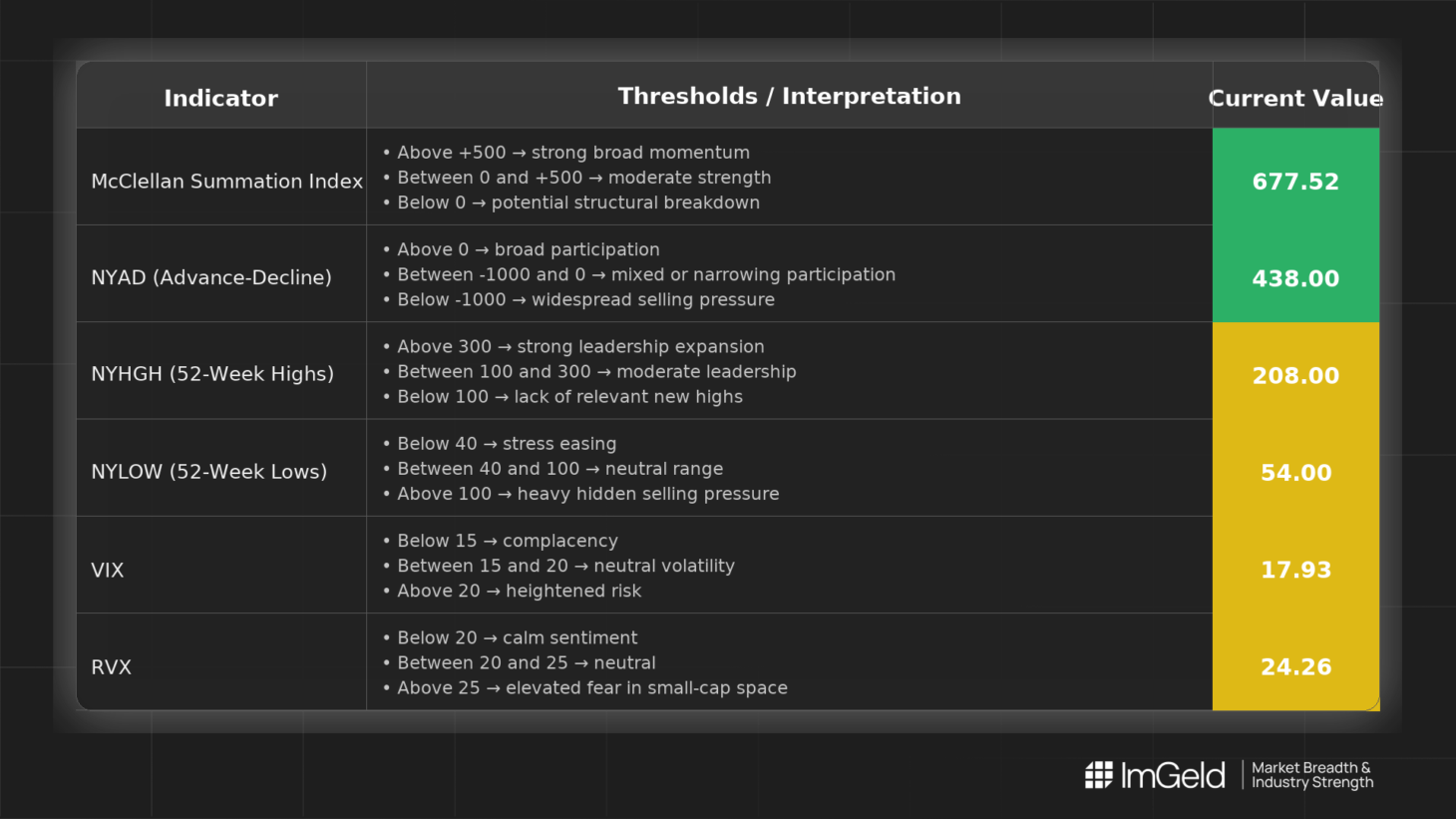

NYSI (McClellan Summation Index)

Structure plateaued then declined (696.72 to 677.52). Momentum faded in the last two sessions, keeping the intermediate trend cautious. A rebuild in thrust is needed to validate further risk-on.

NYAD (Advance–Decline Line)

Daily participation strengthened: four positive readings, including strong prints (839, 438). This indicates buyers are re-engaging beyond a narrow leadership group.

NYHGH (New 52-Week Highs)

Leadership expansion is evident, rising from 136 to 208. More issues are breaking out, a necessary ingredient for durable advances, particularly in mid-caps.

NYLOW (New 52-Week Lows)

Lows spiked mid-period (78) then moderated to 54. Downside pressure persists but is easing, consistent with improving risk appetite.

Volatility Regime

VIX fell to 17.93 and RVX to 24.26, both trending lower. The RVX–VIX spread remains intact, and overall compression favors adding on weakness rather than chasing strength. Lower realized and implied volatility supports selective accumulation in mid-caps.

Tactical Takeaway

Tactical implications: prioritize mid-cap industries where breadth and highs are expanding, notably industrial machinery and automation, semiconductor equipment suppliers, and software infrastructure. Short setups remain more attractive in large-cap defensives and crowded index heavyweights showing narrowing breadth and momentum decay.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.