Are you positioned if NYSI stalls, NYAD rolls over, and VIX re-expands?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-04-04

Executive Summary Date: 2026-04-05

Breadth signals are mixed with a mild negative tilt. The NYSI (McClellan Summation Index) has stalled and edged lower, while NYAD (Advance–Decline Line) printed three down sessions out of five with a net weekly decline. Volatility firmed into the close of the period, with VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) re-expanding after mid-week compression. Tactically, long opportunities may be emerging only in highly selective mid-cap industries showing persistent new highs and constructive pullback behavior. Short setups remain valid in large caps where leadership is concentrated and unconfirmed by breadth; prioritize fading strength in index-heavy names that fail to generate follow-through.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation remains narrow. A brief mid-week improvement in leadership breadth (NYHGH) was not sustained, indicating rotation remains tentative and leadership concentrated. Volatility compressed mid-week and re-expanded into 2026-05-04, arguing for tighter risk controls. A mild divergence is present: NYSI is relatively stable but ebbing, while NYAD turned firmly negative on balance. The five-day pattern remains mixed, signaling digestion rather than clean accumulation or a confirmed continuation. Selectivity is paramount, with an emphasis on relative-strength mid-caps and disciplined short exposure in crowded large caps.

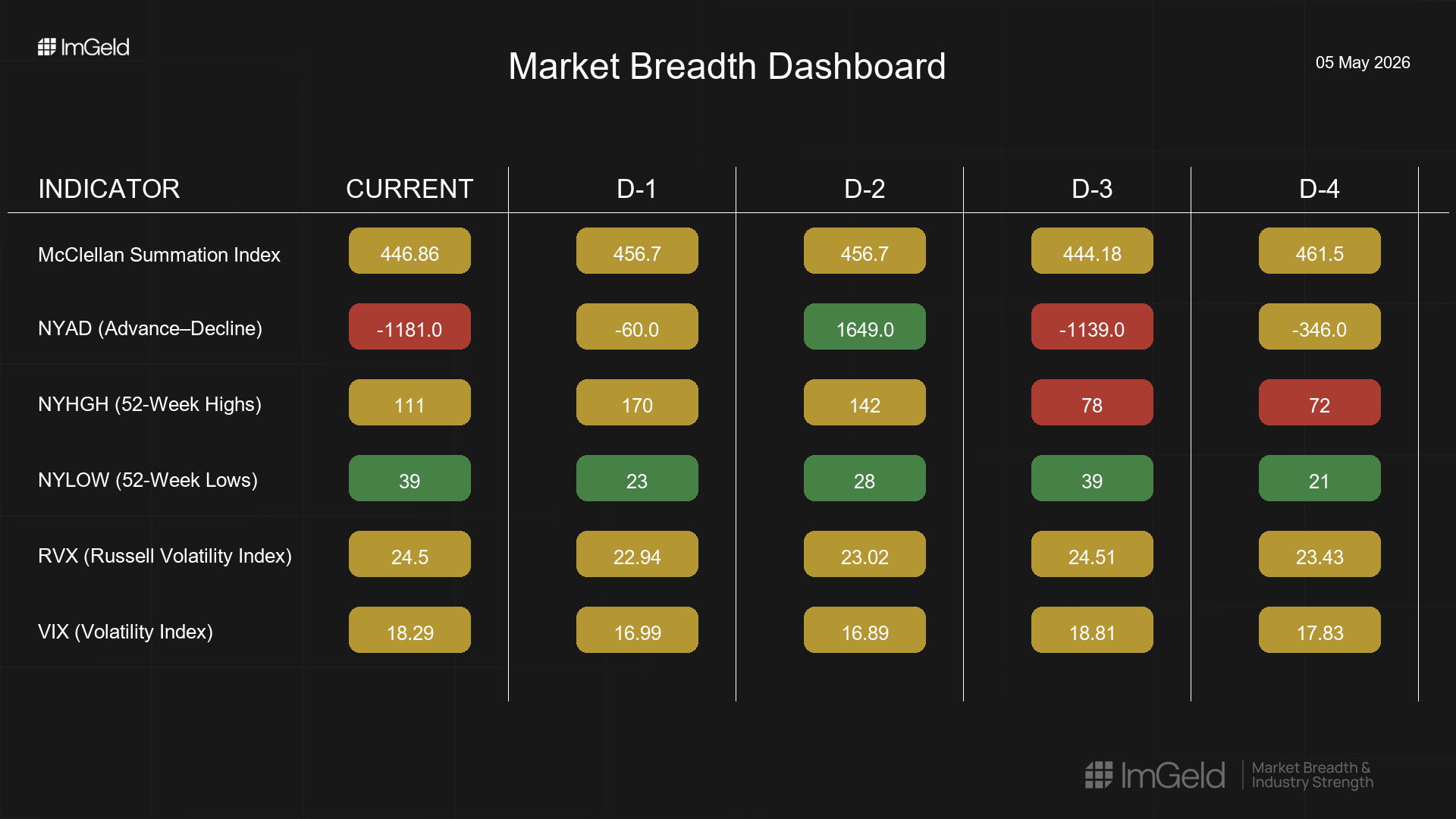

Indicator Breakdown

NYSI (McClellan Summation Index) Structure is plateauing with a slight decline: 461.5 → 444.18 → 456.7 → 456.7 → 446.86. Momentum failed to make a higher high and faded into the last session, indicating waning thrust.

NYAD (Advance–Decline Line) Participation weakened on balance: -346, -1139, +1649, -60, -1181. The strong single up day was more than offset by two broad negative days; net breadth over five sessions is negative, confirming narrower participation.

NYHGH (New 52-Week Highs) Leadership expansion was brief: 72 → 78 → 142 → 170, then cooled to 111. New highs remain above early-week levels but the rollover suggests leadership is not broadening decisively.

NYLOW (New 52-Week Lows) Downside prints stayed contained but ticked up at inflection points: 21 → 39 → 28 → 23 → 39. Risk appetite is intact but fragile, with late-week deterioration warranting caution.

Volatility Regime VIX moved 17.83 → 18.81 → 16.89 → 16.99 → 18.29; RVX 23.43 → 24.51 → 23.02 → 22.94 → 24.50. After mid-week compression, both curves re-expanded, consistent with choppy tape and higher gap risk. This argues for measured gross exposure, tighter stops, and preference for names with clean liquidity profiles.

Tactical Takeaway

Longs: Focus only on mid-cap industries exhibiting consistent new-high cadence and constructive consolidations (e.g., select specialty industrials, electrical equipment, and defense suppliers with stable relative strength). Favor add-on entries on controlled pullbacks rather than breakouts.

Shorts: Large-cap leadership that is index-heavy and breadth-unconfirmed remains vulnerable on rallies; prioritize mean-reversion shorts where volatility is rising and advance–decline fails to confirm price.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.