Breadth Narrows, Volatility Expands: Neutral Bias, Select Mid-Cap Longs, Fade Large-Cap Growth

ImGeld Market Breadth Update | Date: 2025-11-13

Executive Summary

Portfolio bias: NEUTRAL.

Breadth: NYSI (McClellan Summation Index) advanced through mid-week but rolled over on the last session; NYAD (Advance–Decline Line) turned decisively negative, leaving the five-day window net negative.

Volatility: VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) compressed early and then expanded into the close of the period.

Tactically, selective long opportunities are emerging in resilient mid-cap industries that sustained leadership into mid-week, while short setups remain valid in weakening large-cap growth industries. Selectivity should remain high.

Global Read

Participation broadened early in the week but narrowed sharply into the final session. Leadership rotated and became more concentrated by week end, with mid-week strength failing to carry. Volatility transitioned from mild compression to expansion. A divergence emerged as NYSI improved into Thursday while NYAD finished the period net negative. By the five-day consistency rule, signals remain mixed. The pattern suggests early accumulation fading into stalling risk, not a clean continuation.

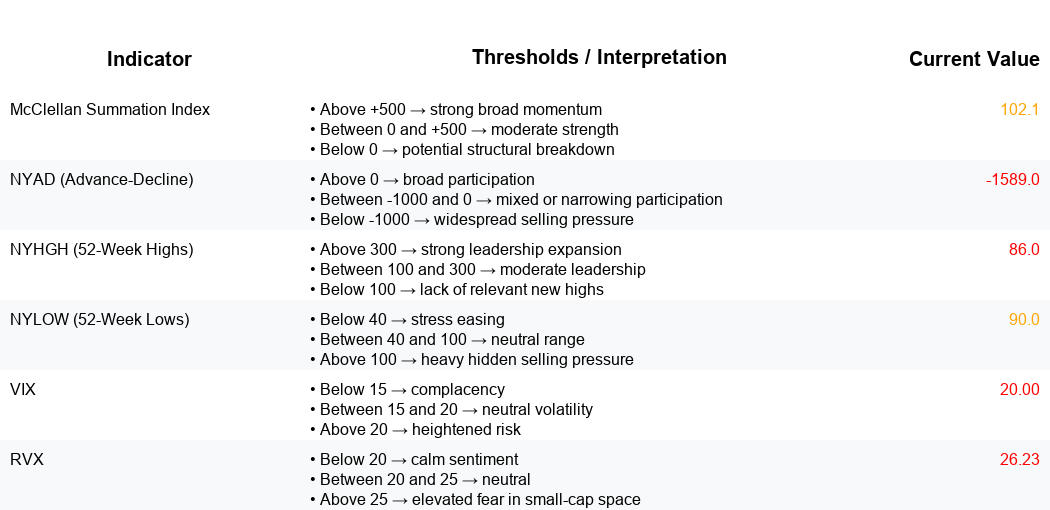

Indicator Breakdown

1. NYSI (McClellan Summation Index)

Structure improved from Monday to Thursday, then slipped on Friday’s close to a still-elevated level. Net-positive over five sessions, but with a near-term wobble that argues for caution.

2. NYAD (Advance–Decline Line)

Day-by-day participation was positive for three sessions, flat once, and sharply negative on the final day. Net deterioration indicates weakening breadth and rising selectivity.

3. NYHGH (New 52-Week Highs)

Highs expanded into mid-week (peak on 11/11–11/12) before retrenching. Leadership expansion stalled, confirming narrowing participation.

4. NYLOW (New 52-Week Lows)

Lows trended down into mid-week, then rebounded. Downside pressure is rebuilding, though not at extremes, signaling moderating risk appetite.

5. Volatility Regime

VIX rose back to ~20 and RVX to ~26, shifting from early-week calm to late-week expansion. This argues for tighter risk controls, staggered entries, and a bias to fade extremes rather than chase breakouts broadly.

Market Breadth Summary

Tactical Allocation Guidance

Recommendation: Neutral.

Rationale: Mixed breadth (NYSI up but rolling, NYAD net negative), leadership narrowing, and expanding volatility favor balance and patience.

Long setups: Focus on mid-cap industries (3–10B market cap) that preserved relative strength and contained drawdowns on 11/13, such as select Software infrastructure, Aerospace and defense suppliers, and niche Specialty chemicals. Favor pullback entries within established uptrends; avoid chasing breakouts that lacked confirmation from NYAD.

Short setups: Remain valid in large-cap growth industries showing distribution under higher volatility, including Internet and interactive media and Semiconductors, and in cyclically sensitive groups if NYLOWs continue to build. Look for failed bounces and breakdown retests for entry timing.

Selectivity: High. Momentum continuation is limited to a few resilient mid-cap groups; mean-reversion has the near-term advantage given the late-week breadth reversal and volatility expansion.

Caution: Volatility conditions are unstable; execution discipline is critical.

CTA

Market breadth is only the starting point.

Thinking of going long or short without knowing which industries are accelerating or breaking down?

Each industry moves in its own rhythm.

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.